Save BIG on Your Mortgage: How Builder Incentives Can Help

Are you looking to save big on your mortgage without sacrificing your dream home? This blog will explore how builder incentives can significantly reduce your monthly payments and overall mortgage costs. Discover the strategies that can help you cut costs and make your home purchase more affordable!

Table of Contents

- Introduction to Builder Incentives

- Understanding Builder Advertisements

- The Importance of Interest Rates

- Maximum Allowable Contributions Explained

- How to Use Builder Money

- Understanding Discount Points

- Exploring Forward Commitments

- The Power of VA Loans

- Real-Life Scenarios: Calculating Savings

- Analyzing Different Home Prices

- Understanding Temporary Buy Downs

- The Role of Personal Financial Strategy

- Evaluating Down Payment Options

- Conclusion and Next Steps

- FAQs

Introduction to Builder Incentives

Builder incentives are financial perks offered by home builders to encourage buyers to choose their properties. These incentives can take various forms, such as reduced closing costs, lower interest rates, or cash bonuses that can be applied toward the purchase. Understanding these incentives can significantly impact your mortgage costs and overall financial commitment.

Types of Builder Incentives

- Closing Cost Assistance: Builders may cover a portion of your closing costs, which can save you thousands of dollars upfront.

- Interest Rate Buydowns: Some builders offer to buy down your interest rate, meaning you pay less in interest over the loan's life.

- Cash Incentives: Builders might provide cash bonuses that you can use as a down payment or for upgrades in the home.

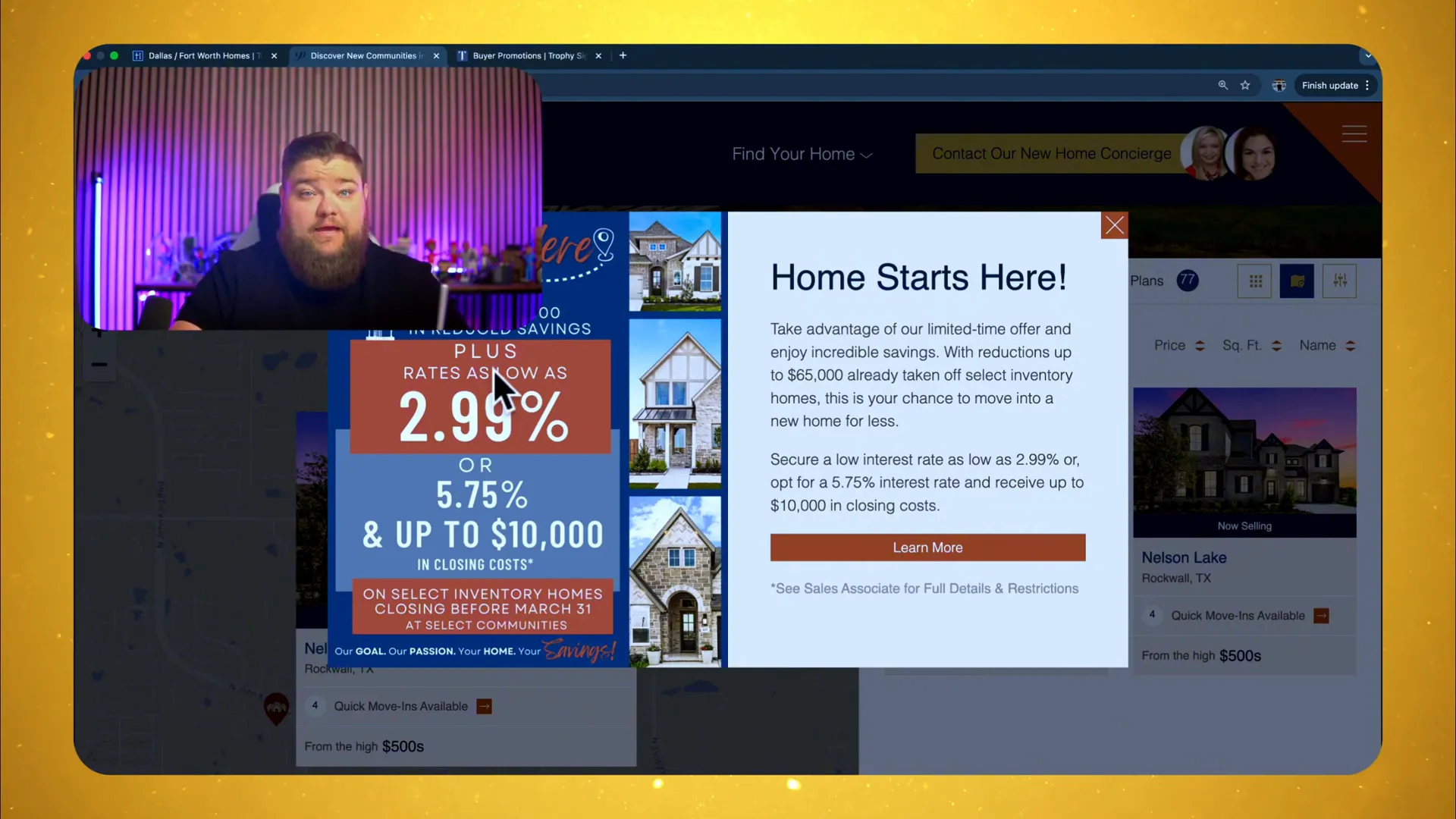

Understanding Builder Advertisements

When browsing builder advertisements, it’s essential to look beyond the eye-catching numbers. While attractive interest rates and cash offers are enticing, understanding the fine print can reveal whether these deals are genuinely beneficial.

Key Aspects to Consider

- Promotional Periods: Check if the rates are promotional and whether they will increase after a certain period.

- Inventory Limitations: Some offers may only apply to specific homes or inventory levels, limiting your choices.

- Qualifying Requirements: Ensure you meet the necessary qualifications to take advantage of the incentives.

The Importance of Interest Rates

Interest rates play a crucial role in determining your monthly mortgage payment. A lower interest rate can lead to significant savings over the life of the loan, making it vital to explore options that builders offer to reduce rates.

How to Secure Lower Interest Rates

- Negotiate with Builders: Don’t hesitate to ask builders for better rates or additional incentives.

- Shop Around: Compare offers from various builders to find the most favorable terms.

- Consider Discount Points: Buying points to lower your interest rate can be a smart financial move if you plan to stay in your home long-term.

Maximum Allowable Contributions Explained

When utilizing builder incentives, it’s essential to understand the concept of maximum allowable contributions. This term refers to the limits set by lenders on how much a builder can contribute to your closing costs or down payment.

Contribution Limits by Loan Type

- Conventional Loans: Less than 10% down - max of 3%, 10% to 24% down - max of 6%, and 25% or more - max of 9%.

- FHA Loans: Up to 6% in contributions.

- VA Loans: 4% plus standard closing costs, allowing for significant savings.

How to Use Builder Money

Understanding how to effectively use the builder's money can lead to substantial savings. Whether it’s through interest rate buy-downs, closing cost assistance, or cash incentives, leveraging these offers can make your home purchase more affordable.

Strategies for Maximizing Builder Money

- Prioritize Needs: Decide whether to use builder money for a lower interest rate or to cover closing costs based on your financial situation.

- Consult with Lenders: Work closely with your lender to determine the best allocation of builder incentives to maximize savings.

- Utilize Flex Cash: If offered, use Flex Cash wisely to enhance your financial position during the loan process.

Understanding Discount Points

Discount points are an effective way to reduce your mortgage interest rate. By paying upfront, you can secure a lower rate, which translates to lower monthly payments and significant savings over time.

Calculating Discount Points

- 1 Point = 1% of Loan Amount: For a $400,000 loan, one point costs $4,000.

- Rate Reduction: Each point typically reduces your interest rate by approximately 0.25%.

- Evaluate Long-Term Savings: Consider how long you plan to stay in the home to determine if buying points is worth it.

Exploring Forward Commitments

Forward commitments are agreements that allow builders to lock in interest rates for future buyers, providing a sense of security in a fluctuating market. This can be particularly beneficial in today’s economic landscape.

Benefits of Forward Commitments

- Price Protection: Locks in your rate, protecting you from future increases.

- Flexibility: Allows you to plan your finances better, knowing your rate won’t change unexpectedly.

- Encourages Home Buying: Builders can sell homes more effectively when buyers feel secure about their financing.

The Power of VA Loans

VA loans are one of the most advantageous financing options available, especially for eligible veterans and active-duty service members. When paired with builder incentives, they can lead to extraordinary savings.

Why Choose a VA Loan?

- No Down Payment: VA loans often require no down payment, making homeownership more accessible.

- No Private Mortgage Insurance: This saves you a significant amount each month compared to other loan types.

- Competitive Interest Rates: VA loans typically offer lower rates, enhancing affordability.

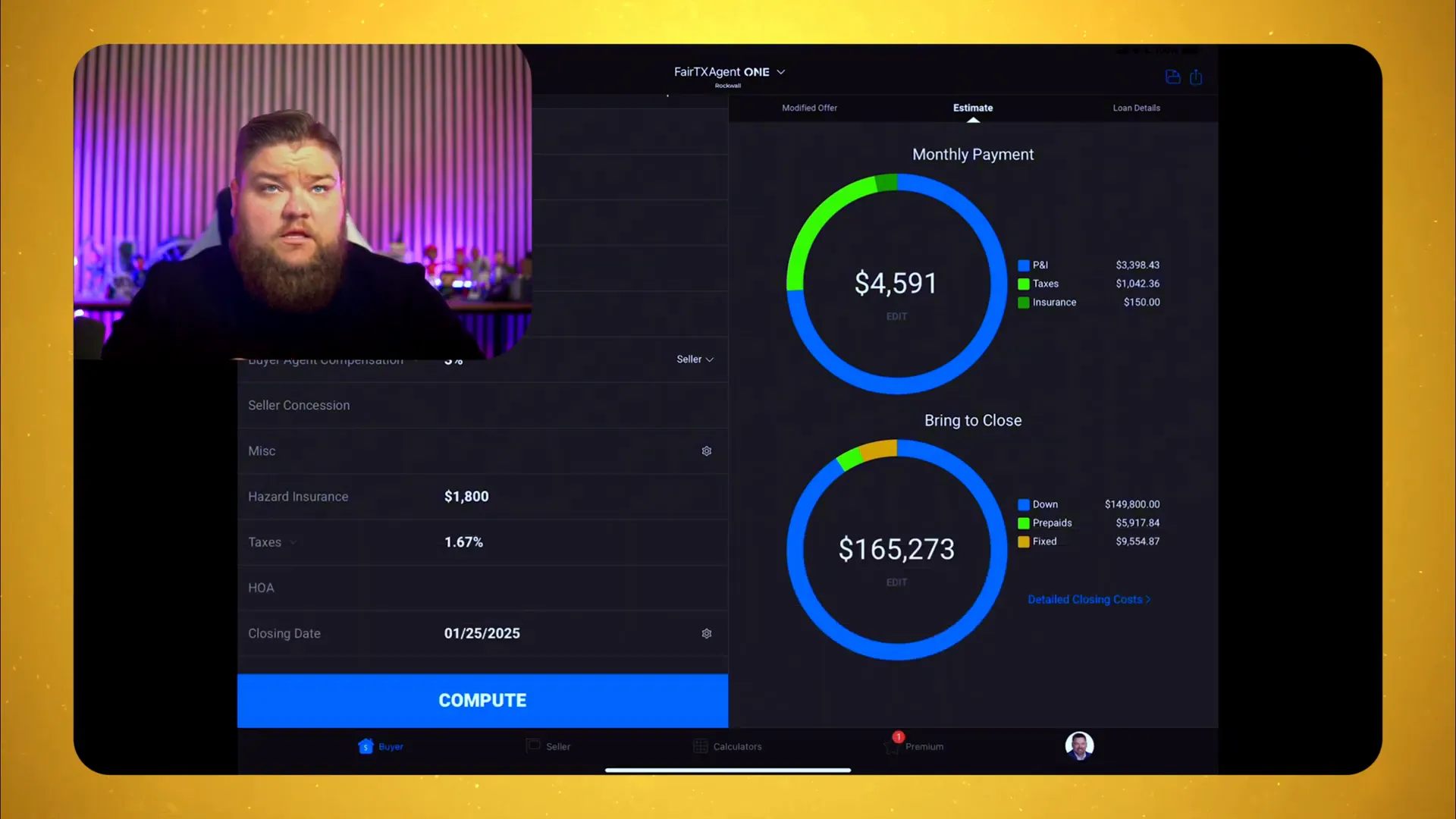

Real-Life Scenarios: Calculating Savings

Understanding how builder incentives can translate into real savings is crucial. Let's break down some scenarios that illustrate potential savings with different home prices and interest rates.

Scenario 1: $750,000 Home Purchase

Imagine purchasing a home priced at $750,000 with a 20% down payment. The prevailing market interest rate is 7.10%. Without any builder incentives, your monthly payment could be approximately $6,376. However, if a builder offers you a fixed interest rate of 5.49% for the life of the loan, your monthly payment drops to around $5,630. That’s a significant reduction!

First Year Savings with Temporary Buy Down

Now, consider a temporary buy down where the first-year interest is set at 4.49%. In this case, your monthly payment could further decrease to about $5,196. That’s a whopping saving of over $1,180 per month compared to the original market rate!

Scenario 2: $525,000 Home Purchase

Let’s look at a more modest home priced at $525,000. With the same 20% down payment and a market interest rate of 7.10%, your monthly payment would be about $4,600. But with the builder's incentive bringing the rate down to 5.49%, the payment reduces to approximately $4,659. This represents a monthly saving of nearly $1,000!

Year One with Temporary Buy Down

Using the first-year temporary buy down of 4.49%, your payment drops to around $3,800, saving you $800 monthly. Over the course of a year, that’s $9,600!

Analyzing Different Home Prices

When considering a home purchase, it’s essential to analyze how different home prices affect your mortgage payment. Let’s explore this further.

Understanding the Impact of Home Price

- Lower Price Points: A home priced at $400,000 with a 5% down payment and a 7.10% interest rate will yield a monthly payment of approximately $3,300.

- Mid-Range Prices: For a $525,000 home, the numbers shift significantly. With incentives, your payments can drop by hundreds each month.

- Higher-End Homes: On homes priced at $750,000, the savings can be substantial, especially with lower fixed rates.

Understanding Temporary Buy Downs

Temporary buy downs are an excellent tool for homebuyers looking to reduce their initial monthly payments. They allow you to start with a lower interest rate that gradually increases over time.

How Temporary Buy Downs Work

- 3-2-1 Buy Down: The first year has a 3% lower interest rate, the second year drops by 2%, and the third year by 1%, before reverting to the standard rate.

- Benefits: This structure allows buyers to ease into their mortgage payments, which can be particularly helpful during the first few years of homeownership.

- Qualification: Borrowers must qualify at the higher interest rate, which is essential in the approval process.

The Role of Personal Financial Strategy

Your personal financial strategy plays a significant role in deciding how to utilize builder incentives effectively. Here are some strategies to consider.

Key Financial Strategies

- Asset Control: Aim to control your home for as little money down as possible. This allows you to keep more cash on hand for emergencies or investments.

- Comfort Level: Choose a down payment that aligns with your comfort level. Whether it's 5%, 10%, or 20%, make sure it fits your financial goals.

- Investment Opportunities: Consider the opportunity cost of your down payment versus potential investments. Keeping cash available could yield better long-term returns.

Evaluating Down Payment Options

Deciding on the right down payment can significantly influence your mortgage terms and overall financial health. Here’s how to evaluate your options.

Down Payment Considerations

- 5% Down Payment: This option keeps your cash flow flexible but may result in higher monthly payments due to private mortgage insurance (PMI).

- 10% Down Payment: A middle ground, this option lowers your monthly payments without a significant cash outlay.

- 20% Down Payment: Avoids PMI, but ties up a large amount of cash. Ensure this aligns with your financial goals.

Conclusion and Next Steps

In summary, builder incentives present a fantastic opportunity to save big on your mortgage. By understanding different scenarios, analyzing various home prices, and strategically planning your down payment, you can maximize your savings.

Next Steps

- Research Builders: Investigate builders in your area and the incentives they offer.

- Consult with Lenders: Speak with mortgage lenders to understand your options and get pre-approved.

- Evaluate Your Budget: Determine how much you can afford and what down payment strategy works best for you.

FAQs

What are builder incentives?

Builder incentives are financial offers from home builders designed to attract buyers, which can include reduced closing costs, lower interest rates, or cash bonuses.

How do temporary buy downs work?

Temporary buy downs allow buyers to start with a lower interest rate for the first few years of their mortgage, which gradually increases to the standard rate.

What should I consider before choosing a down payment?

Consider your comfort level, cash flow needs, and long-term financial strategy when deciding on your down payment amount.

How can I save big on my mortgage?

Utilizing builder incentives, understanding interest rates, and strategically planning your down payment can significantly reduce your overall mortgage costs.

Zak Schmidt

From in-depth property tours and builder reviews to practical how-to guides and community insights, I make navigating the real estate process easy and enjoyable.